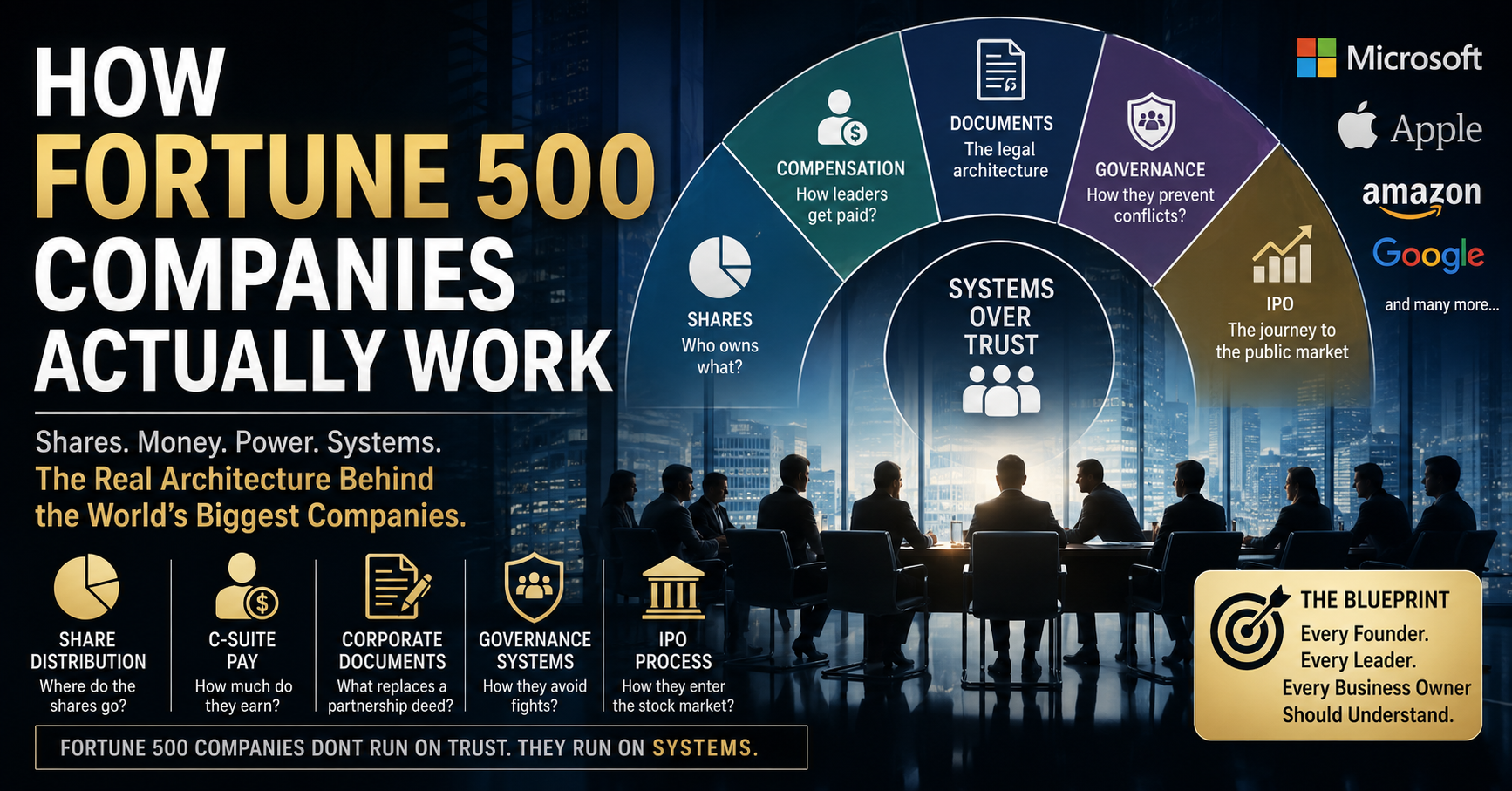

How Fortune 500 Companies Actually Work

PART 1 — WHERE DO THE SHARES GO?

When a founder starts a company, they own 100%. As the company grows, shares get distributed in layers.

The Typical Share Distribution Journey

Stage 1 — Early Company

- Founder owns 80–100%

- Co-founders split remaining %

- Nothing formal yet

Stage 2 — Seed & Early Investors (Angel/VC Rounds)

- Founder gives up 10–30% to early investors in exchange for capital

- This is called equity dilution — your % shrinks but the total value grows

- Example: You own 100% of a $100K company = $100K yours. After giving 20% for $500K investment, you own 80% of a $600K company = $480K yours. You’re richer even though your % dropped.

Stage 3 — Employee Stock Option Pool (ESOP)

- Companies reserve 10–20% of shares for employees

- This is how they attract and retain top talent without paying massive salaries

- Employees get options (right to buy shares at a fixed price later)

- If company grows, their options become worth millions — this is how early Google/Microsoft employees became wealthy

Stage 4 — IPO (Initial Public Offering)

- Company sells shares to the general public on a stock exchange

- Typically 10–30% of total shares are floated publicly

- This raises massive capital and also creates liquidity — founders/early investors can now sell their shares

Stage 5 — Institutional Investors

- Mutual funds, pension funds, hedge funds, sovereign wealth funds buy large blocks

- These are the real “majority owners” of most Fortune 500 companies

So Where Did Bill Gates’ Shares Go?

- Gates founded Microsoft in 1975 owning ~49%

- After IPO in 1986, his stake diluted to ~49% (Microsoft’s IPO was small float)

- Over decades he sold shares systematically to fund philanthropy

- By 2019 he owned less than 1% — not because it was taken, but because he chose to sell

- Same with Bezos — sold billions in Amazon stock annually to fund Blue Origin

- Jobs was actually fired, came back, and took only $1 salary — his wealth was in Apple stock he held

The real answer: Founders don’t lose shares. They sell them, gift them, or dilute through funding rounds — by choice.

Typical Share Distribution of a Mature Fortune 500

| Holder | Typical % |

|---|---|

| Institutional investors (BlackRock, Vanguard, Fidelity) | 60–75% |

| Founder / founding family | 1–15% |

| CEO & C-suite (via stock grants) | 1–5% |

| Employee ESOP pool | 5–15% |

| Public float (retail investors) | 10–25% |

| Treasury stock (company holds its own shares) | Variable |

Vanguard and BlackRock are the actual largest shareholders of most Fortune 500 companies. They own 5–8% of almost every major US company simultaneously through index funds.

PART 2 — HOW MUCH DO THEY PAY C-SUITE?

Fortune 500 CEO compensation is structured in layers — base salary is actually the smallest part.

Typical Fortune 500 C-Suite Compensation Structure

| Role | Base Salary | Annual Bonus | Stock Awards | Total Compensation |

|---|---|---|---|---|

| CEO | $1M–$3M | $2M–$10M | $15M–$50M+ | $20M–$60M+ |

| COO | $800K–$2M | $1M–$5M | $8M–$20M | $10M–$25M |

| CFO | $700K–$1.5M | $1M–$4M | $6M–$15M | $8M–$20M |

| CTO | $700K–$1.5M | $1M–$3M | $6M–$15M | $8M–$18M |

| CMO/CHRO | $500K–$1M | $500K–$2M | $3M–$8M | $4M–$10M |

Real Examples (2023–2024)

- Elon Musk (Tesla CEO): $0 base salary, requested $56B in stock options (courts blocked it)

- Tim Cook (Apple CEO): $3M base + $6M bonus + $75M in stock = ~$84M total

- Satya Nadella (Microsoft CEO): $2.5M base + $5.2M bonus + $39M stock = ~$49M total

- Andy Jassy (Amazon CEO): $1.75M base + $0 bonus + $212M in stock grants (vesting over 5 years)

Why Stock Is the Real Compensation

- Stock vests over 3–5 years — golden handcuffs, they can’t just leave

- Tied to company performance — if stock drops, they earn less

- Tax advantages in US — capital gains tax lower than income tax

- Aligns executive interest with shareholders — if they grow the company, they get rich too

PART 3 — WHAT DO THEIR “PARTNERSHIP DEEDS” LOOK LIKE?

At Fortune 500 level, it’s not a partnership deed — it’s a layered legal architecture.

The Documents That Replace a Partnership Deed

1. Certificate of Incorporation

- Filed with the state (usually Delaware — 67% of Fortune 500 incorporated there)

- Establishes the legal entity, authorized shares, and company purpose

- Delaware chosen because: flexible corporate law, business-friendly courts, privacy

2. Corporate Bylaws

- The operating rulebook of the corporation

- Covers: Board composition, voting rights, meeting procedures, officer roles and removal

- Who can sign contracts, how decisions are made, what requires board approval

- This is the Fortune 500 equivalent of your partnership deed’s conduct section

3. Shareholder Agreement

- Rights and restrictions on share transfers

- Tag-along rights (if majority sells, minority can join)

- Drag-along rights (majority can force minority to sell in an acquisition)

- Anti-dilution protection for early investors

- Voting rights per share class

4. Share Classes — The Key to Founder Control

This is how founders keep control even with 1% ownership:

| Share Class | Who Holds It | Voting Power |

|---|---|---|

| Class A (Common) | Public investors | 1 vote per share |

| Class B (Super voting) | Founders | 10 votes per share |

| Class C | Employees/others | 0 votes |

- Google: Larry Page & Sergey Brin hold Class B shares — 10 votes each vs. public’s 1

- Facebook/Meta: Zuckerberg holds Class B — controls ~57% of voting power with ~13% economic ownership

- This is why founders can own 1% of shares but still control 100% of decisions

5. Executive Employment Contracts

- Role definition, authority limits, compensation structure

- Termination conditions — for cause vs. without cause (huge difference in severance)

- Non-compete, non-solicitation clauses (2–5 years post-exit)

- Clawback provisions — bonuses returned if fraud is discovered later

6. Board of Directors Structure

- Shareholders elect a Board (typically 7–12 members)

- Board hires and fires the CEO — even a founder-CEO can be removed by the board

- Board approves major decisions: acquisitions, debt, equity issuance, executive pay

- Independent directors required by law (majority must have no company ties)

- Steve Jobs was famously removed by his own board in 1985

PART 4 — HOW THEY AVOID FIGHTS (GOVERNANCE SYSTEMS)

This is what most people miss. Fortune 500 companies don’t avoid fights through trust — they avoid fights through systems that remove the need for trust.

The 5 Systems That Prevent Fights

1. The Board Acts as a Referee

- No single person, including the CEO, has unchecked authority

- Major decisions require board approval — removes “my word vs. your word”

- Independent directors have no loyalty to either side — they rule on facts

2. Separation of Ownership and Management

- Shareholders own the company but don’t run it

- Board oversees strategy but doesn’t operate it

- C-suite operates it but doesn’t own decisions above their mandate

- Three layers = three checks. No one person can hold all power.

3. Documented Decision Thresholds

- Every level has a defined spending and decision authority

- Manager: approve up to $10K

- VP: up to $100K

- C-suite: up to $1M

- Board: above $1M or strategic decisions

- Nothing is left to verbal agreement or “ask the boss”

4. Audit Committees

- Separate committee of board members (must be independent)

- Reviews all financial statements before they’re published

- External auditor reports to them — not to the CEO

- Removes the ability for management to manipulate financial information quietly

5. Legal Counsel on Retainer

- General Counsel (Chief Legal Officer) sits at the executive table

- Every agreement, contract, and decision of size goes through legal review

- Nothing significant is “figured out later”

Specific Anti-Fight Clauses in Corporate Documents

- Indemnification Clauses — company protects directors/officers from personal liability for good-faith decisions

- Business Judgment Rule — as long as a decision was informed and in good faith, courts won’t second-guess it

- Fiduciary Duty — every officer/director is legally bound to act in the company’s best interest, not their own. Breach = personal liability.

- Clawback Provisions — Dodd-Frank Act (US law) requires Fortune 500 to reclaim executive bonuses if financials are later found to be misstated

- Whistleblower Protections — internal employees can report wrongdoing without retaliation — creates self-policing culture

PART 5 — HOW THEY ENTER THE STOCK MARKET (IPO PROCESS)

The Full IPO Journey

Step 1 — Internal Decision (1–2 years before IPO)

- Board and founders decide: is the company ready?

- Requirements: consistent revenue growth, audited financials (3 years), strong governance, scalable business model

- Appoint investment banks as underwriters (Goldman Sachs, Morgan Stanley, JPMorgan)

Step 2 — Due Diligence & Audit

- External auditors verify every financial statement

- Legal teams review all contracts, IP, litigation, liabilities

- This is the most intensive phase — nothing hidden survives this

Step 3 — S-1 Filing (Registration Statement)

- Filed with SEC (Securities & Exchange Commission)

- Public document — anyone can read it

- Discloses: business model, financials, risks, ownership structure, how IPO proceeds will be used

- Pakistan equivalent: SECP filing with PSX (Pakistan Stock Exchange)

Step 4 — Roadshow (6–8 weeks)

- CEO and CFO travel to major financial centers (New York, London, Hong Kong)

- Present to institutional investors — pension funds, hedge funds, mutual funds

- Purpose: generate demand before shares are priced

Step 5 — Pricing

- Based on demand from roadshow, underwriters set the IPO price

- If demand is 10x the available shares (oversubscribed), price goes higher

- Under-subscription = price drops or IPO delayed

Step 6 — First Day of Trading

- Shares listed on NYSE or NASDAQ

- Opening price determined by market supply and demand

- Company receives IPO proceeds (primary offering) — subsequent trading doesn’t give company money directly

Step 7 — Lock-up Period (180 days)

- Founders and early investors cannot sell their shares for 6 months post-IPO

- Prevents insiders from dumping shares immediately after public buys in

- After lock-up expires — the first big selling wave often happens

What the Company Gets vs. What Shareholders Get

- Company gets: Cash from newly issued shares (used for growth, debt payoff, expansion)

- Existing shareholders get: Liquidity — they can now sell their shares on the open market

- Public gets: Ownership stake and future upside

The One Mental Model That Ties All of This Together

Fortune 500 companies don’t run on trust between people.

They run on systems that make trust unnecessary.

- Documents define authority so no one needs to ask

- Boards create accountability so no one is above consequences

- Share structures protect founders without requiring loyalty

- Compensation tied to performance removes misaligned incentives

The reason your 2-person agency partnership needs a good deed is the same reason Microsoft has 400 lawyers on staff — the bigger the money, the more important the paperwork.